Letting your winners run is for chumps (sometimes)

Letting your winners run is for chumps (sometimes)

A purposeful approach to rebalancing, exiting, and cutting losers.

I’m a big believer in the idea of there being a right and wrong way of doing things. Sure, there are shades of grey, and we will make many mistakes in our methodologies, but if you’re investing someone else’s money (or even your own), you should at least be making decisions with purpose. Decisions should never be a gut feeling— they should be well thought through. So I LOVE when people point out the contradictions of finance platitudes because I usually just think one of them is wrong.

(Edwin writes a great newsletter that you should definitely check out btw)

There are very successful investors on each side of these topics. And one of the most conflicting topics in finance is when to exit positions. "Cut your losers, let your winners run" is thrown around almost as much as "buy low sell high," but successful investors (including Seth Klarman) advise to sell just a little below fair value so you know you'll find a buyer. Most of the analysis I’ve seen on this topic is half-baked and relies on either (a) anecdotes, (b) platitudes, or (c) scapegoat-ing it to personal preference and style.

“Let your winners run” is somewhat useless advice. It rarely offsets mistakes, adds ambiguity, and doesn’t answer the key questions: how long you should let them run, and when should I rebalance and/or take profits? Luckily, there is a mental framework we can use to figure out what you should be doing in your portfolio. Today, I want to lay out that process for long positions.

Dealing with positions over time:

After you put a position on, three things will change over time:

Your thesis is either going to be proven right or wrong, changing the probability you would assign to upside / downside scenarios

The forecasted risk / return of the position changes as the spot price gets closer / further away to the upside and downside scenarios

The position naturally changes weighting in your portfolio as it grows or shrinks, and as the rest of your portfolio grows or shrinks

As we've discussed before, the core of portfolio management is creating a probability-weighted return distribution, and then using it to properly size each bet. Notice that each of these forces pull our sizing calculation in a different direction. In a winning position, the thesis is being proven correct makes our probabilities skew upwards. This can happen both (a) because good news related to your catalyst is what drove the stock up, or (b) because the stock went up for no apparent reason, potentially indicating others have begun to believe in your thesis, thereby giving it more credibility. But your upside scenario is also becoming (in percent terms) less and less attractive, while you're downside (in percent terms) is becoming more and more daunting.

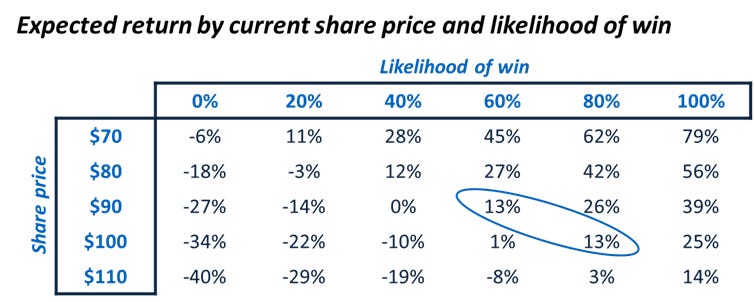

These dynamics obviously offset each other to some degree. Let's take a situation where you have a company in ongoing litigation trading at $100 per share. You think if they win the case (which you believe has a 2/3 chance of happening1), the stock will go to $125 per share. But if they lose (which you believe they have a 1/3 chance of doing), the shares will go down to $66.

Assuming the underlying upside / downside don’t change, the two major levers that will impact our expected return is (a) the spot price, and (b) the estimated percent chance they win litigation. If we map these two axis onto a table, we can begin to see the interplay between the two:

Note that at points on this table (an example is contained within the blue circle), an increase in share price can be offset by an increase in likelihood-of-a-win. But all else being equal, the expected return of an investment will increase with the likelihood-of-a-win, and decrease with an increase in share price.

Implications to sizing

As we've discussed before, there is a simple way to correctly size positions known as the Kelly Criterion2. By plugging in our upside scenario, downside scenario, and probability weightings we can understand what portion of our portfolio to allocate to any given bet.

We are most likely to think about sizing positions when we first put a position on. But in reality, this same tool can be again and again to rebalance a position, and decide when to exit it. Here is how it works:

Before you put on a position, create an estimated probability-weighted return distribution

Calculate Kelly with either the actual formula (if in a binary scenario) or by running a simulation of returns, looking to maximize the Median long term CAGR

Size the position with some proportion of Kelly (I have seen preferences anywhere from 1/4 to 3/4 here)

As the position evolves, continue to update your scenario probabilities and recalculate proper weighting when given new inputs (primarily Risk/Return based on new stock price, and probability weightings, but also upside downside scenarios if applicable)

If the sizing in your portfolio becomes materially different from the required weighting, rebalance your portfolio.

If the recommended sizing reaches zero, close out of the position

Implications to portfolio management

So let’s say all of the above makes sense to you, but you hate dealing with probabilities— you just want to know what this process implies re: dealing with long positions. Well, let’s first look at dealing with winners:

Winning positions

I know I’ve been bashing on heuristics, but this strategy generally does recommend investors to let their winners run. This is because if you’re a fundamental investor looking for high-quality companies, the upside scenarios and confidence in management’s ability to execute are only going to improve over time. This is hopefully offset by a rising stock price.

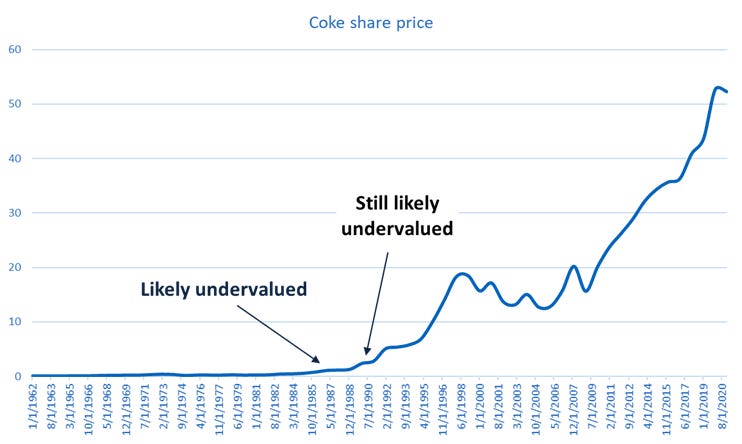

For example, if Coca-Cola was an attractive and undervalued stock in 1987 at $2.50 a share— the upside to fair value might have been only $3 - $4. But it was likely still undervalued when it hit $5 in 1990 because the fair value had moved higher in parallel. In these situations, the stocks can keep going up for years before this methodology will tell you to exit the position. If you read enough about portfolio management, you’re bound to find a number of sources that agree with this. The Art of Execution doesn’t even talk about dealing with winning positions outside of letting winners run. But this is a good underlying framework to keep in mind when digesting those sorts of materials.

Additionally, Kelly generally recommends that you rebalance your positions in the interim. Suppose you determined that the proper weighting of Coke was 25% in 1987, theoretically, the position could have reached to be >60% of your portfolios allocation by 1990 if you let the position run. The proper thing to do would be to gradually take some profits over time to keep the position size back in the Kelly-prescribed range. Practically, it is hard to rebalance continually due to non-zero execution costs. But rebalancing daily, weekly or monthly are all okay depending on the variance you are willing to accept into your portfolio.

In some rare situations, the growth of our confidence in a position will outpace the upward movement in the stock. Given markets are at least somewhat efficient, it is not likely that material news is repeatedly released with no market reaction. However, it does sometimes happen, and in these rare situations, the Kelly methodology implies that it makes sense to average up into positions. But if you find yourself continually averaging up over and over again, it likely indicates you’re prone to experiencing thesis creep.

At other points, the stock will either become “expensive” versus our upside scenario, our confidence will waiver for one reason or another, or a new risk will emerge that materially impacts the downside. In these situations, you should likely reassess your original thesis and begin to take money off the table.

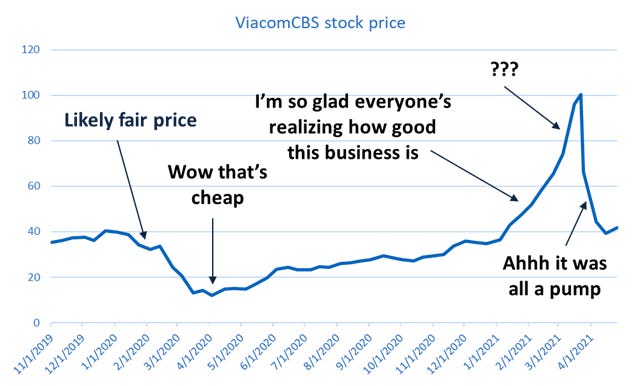

One last point— there several PMs I’ve spoken to about rebalancing that point to the momentum return premia as a reason to let winners run. I think this is a poor way of looking at the world. Statistics is often a great way of describing events but is a poor rationale for a stock to go up. There are two fundamental reasons for a stock price to increase: (a) an economic increase in value (this can impact both EPS and P/E measurements, but always deals with intrinsic value), and (b) an increase in market value often caused by capital flows (also called a mania). These two forces are most often intertwined, with a rapid increase in intrinsic value leading to an increase in market participation which becomes it’s own catalyst for further price swings (though sometimes the former isn’t required— see $GME).

The momentum factor conflates these two forces. The market reflects economic increases in value over time, which is then reflected in momentum as “stocks that go up continue to go up”. But given that when you reach your upside valuations, you’ve implicitly eaten up the economic part of momentums impact. All that is left then is mania driving the stock higher. Can mania be very profitable? Yes. Is mania easy to predict? No. The downside risks also start getting bigger and bigger as when manias disappear so does the liquidity.

So all that being said, unless you want to add some trend-following flavors to your portfolio, I would suggest getting out when the economic reason you got in is no longer an attractive wager. Simple enough? Let’s move on to losers.

Losing positions

The second most popular piece of advice I hear after “let your winners run” is “cut your loses quickly”. But as most value investors know, if you like something at $10, you should like it even more at $5. Warren Buffett does this, so does Seth Klarman. But Paul Tudor Jones thinks they’re both losers.

Let’s go back to our original three levers. when a position moves against us, three things happen:

Our confidence in the position is shaken. There are also likely more psychological effects from this, but that is well out of scope for this blog

Our downside decreases— it can only go to $0 (unless you’re selling options of course) — and our upside increases, that is, if our scenarios remain intact

It becomes a smaller proportion of our portfolio.

Let’s start with the confidence point.

If we start to lose money on a position, it is often on the back of bad news. If you see that things are headed for the downside scenario, you need to get out immediately. At some point this becomes loss mitigation more than portfolio management. Now let’s say the news is only slightly bad, and you think the market is overreacting. In this situation you need to balance whether the decrease in probability is offset by the increase in upside scenarios. The answer may be yes, or it may be no, but it is almost never “do nothing”.

Let’s instead say that we can’t find any news at all. In this situation we still need to shift our confidence levels downwards. This is because (a) we are all human, and there can be a flaw in even the deepest diligence work3, and (b) the other big market participants out there generally have also done a lot of work, and if they have the ability to push the stock lower, you need to ask who is on the other side? Do they know more than we ever can?

The big question is how much do we need to reduce our confidence by, and is it enough to offset the increasingly attractive upside. This is another situation when the answer might be yes or no, but it is almost never correct to do nothing.

I would also caution that a falling stock price can become a catalyst for new unforeseen downsides. If a company can no longer refinance with convertibles, for example, it could precipitate a credit quality decrease, which can impact it’s supply chain, it’s financing ability, and also it’s ability to remain solvent. Other times, slightly bad news can have a butterfly effect on a company. If you thought the downside for a mining company was the SOTP of it’s mineral holdings, and then the value of commodities starts to slip, there is a non-zero chance the company becomes unprofitable, has liquidity issues, and has to restructure. All while it remains solvent.

Because of this dynamic downside risk, John Hempton of Bronte believes you should avoid averaging down in over-levered or cigar-butt type companies. I think that those rules are overly simplified to the point of being useless. As long as you are appropriately thinking about downside scenarios, you should be capturing 90%+ of the downside risks in your original sizing. As things change, having a potential 100% downside is scary, but can be properly reflected with Kelly.

Of course, for downward movement that are just noise, none of this matters. When the market is down 1% and the position is down .7%, you probably don’t need to worry so much about upsides and downsides and probabilities. Just rebalance your portfolio and be on your way.

Other thoughts on rebalancing

It’s worth mentioning here that rebalancing a long position is basically free money that many simply ignore.

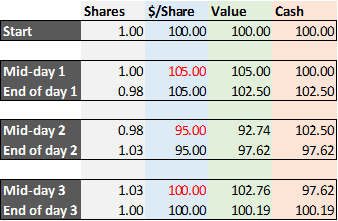

Let’s say a stock trades at $100 per share, and you want it to be ~50% of your portfolio (this is obviously an exaggerated number, please don’t run a portfolio that concentrated). Let’s also say that you have a price target in mind of $150 a share, and no daily movements will change your conviction that that number is correct.

Let’s say one day the stock goes up 5% (or $5) to $105 per share. Assuming nothing else happens in your portfolio, this stock is now 51.2% of your portfolio. Obviously, we need to rebalance, so on market close you sell .02 shares at $105 to bring it back to a 50% allocation. You now hold $102.5 in stock (.98 shares) and have $102.5 in cash.

But the next day the stock goes down, all the way to $95 per share, it is now only 48% of your portfolio. Once again we need to rebalance, and so on market close we buy back shares. This is great news, because the next day, the stock rebounds back to $100 per share. Once again, we rebalance. Notice that at the end of all this, the stock is back at $100 per share, but we actually now have made .2% by doing nothing but rebalancing!

This is why rebalancing is so important. By doing nothing but naively selling a little bit as it goes up, and buying a little more as it goes down, we can add significant alpha to our portfolios. That is a major piece of Kelly’s Alpha.

I hope to eventually write a more in depth piece on the different ways to forecast events, but the basis is using both frequentism (how often do similar events happen in the past) and Bayesian math to come to some educated guess.

I always have to laugh when I think about the failure of massive mergers. Like if Verizon can’t see that Yahoo was a bad business even after spending millions on the diligence, then the rest of us likely aren’t much better.

Hi Hawnk,

I think this is probably the most nuanced, insightful and _practically helpful_ piece on rebalancing I've ever read - thank you very much. I've really enjoyed everything you've written so far.

I had a few questions in case you were looking for material for future posts (or want to answer here):

1) As you say in your "Diversifying Wrong" article, using Kelly necessarily implies rebalancing (so useful to see that so clearly expressed!). I completely follow your arguments, which make intuitive sense. Do you have any comments on this 2020 article, which found that increasing the frequency of rebalancing increased performance but at the expense of also increasing risk and (obviously) trading costs?

--- Practical Implementation of the Kelly Criterion: Optimal Growth Rate, Number of Trades, and Rebalancing Frequency for Equity Portfolios, https://www.frontiersin.org/articles/10.3389/fams.2020.577050/full

2) It would be brilliant to look at a practical how-to of position sizing and concentration in an overall portfolio. For a non-specialist, the maths can be rather forbidding. Do you have any heuristics to help here, for example on maximum sizes given the tendency of Kelly portfolios to be highly concentrated?

--- This Github Python code helps construct a Kelly optimal portfolio based on the user's expected returns and percentage of full Kelly desired. It then calculates the historical covariances (assuming these will be the same going forward...) to determine the optimal portfolio weightings. Would be really interested to hear your thoughts on an approach like this.

https://github.com/thk3421-models/KellyPortfolio

3) In your "Half Kelly" article you began by pointing out that institutional investors must "find ways to grow their assets under the vast majority of scenarios" and therefore need to avoid lottery tickets as well as Russian Roulette. What would be the circumstances and methods for an unconstrained investor to act differently from an institutional one in order to maximise terminal wealth? Or is the institutional approach "the right way of doing things"? :-)

4) Just spotted a few typos in your articles on it's vs its.

As I said, I'm finding your pieces hugely insightful and am very much looking forward to the next one. If you have any recommended sources, books, articles to better understand this puzzle, those would also be widely appreciated I'm sure!

Thanks again