Maximizing the downside: Why practitioners halve Kelly

Maximizing the downside: Why practitioners halve Kelly

TLDR: Optimizing for robustness >>> optimizing for returns

Introduction

If portfolio management is the art of sizing, then the Kelly Criterion is our golden ratio. Understanding the dynamics of Kelly can give PMs a way to understand how their portfolios should be rebalanced, resized, and dynamically changed over time.

But as I’ve mentioned previously, practitioners don’t always use the full Kelly. Instead, practitioners often use only a portion of Kelly – often somewhere between ½ - ¾ – in in their position sizing. There are several reasons to do this, and today I want to dive into them.

The three main reasons are

the maximization of worst-case scenarios,

the impact of unforeseen risks, and

the impact of uncertainty

The maximization of worst-case alternate realities

Imagine for a minute that parallel universes existed. Every time you flipped a coin, the world split in two, and there is one universe where it's heads and another where it's tails. And imagine this happens again, and again. Now imagine we had to solve for not just the best possible outcome, but for all possible outcomes—wouldn’t this change the way we behave?

Take two games here for example; Russian roulette and the lottery.

If we decided to play Russian roulette for $1M (that is, you put a single bullet in a gun, put it to your temple, and pull the trigger— you have a 1/6 chance of dying, and if you survive, you are paid $1M), we are trading a horrible 1/6th percentile outcome, for a hugely beneficial outcome in 5/6th realities. But this isn’t a logical game to play—in fact, no sane person would take this risk.

In the lottery, we are doing the exact opposite—we are maximizing the top 1/100 million percentile, at the very minor cost of the other 99%+ of outcomes.

Fiduciaries (i.e., institutional money managers) are often looking to avoid either of these games. Their job is to not lose money, and then hopefully make a little bit of money in all scenarios. They cannot play Russian roulette with their assets, and they cannot buy lottery tickets. What instead they must do is find ways to grow their assets under the vast majority of scenarios. Let’s use an example to show the implications:

Let’s say we have a 6-sided dice game1 with the following odds:

If we roll a 1: we lose 25% (~.167 chance)

If we roll a 2, 3, or 4: we gain 1% (~.667 chance)

If we roll a 6: we gain 25% (~.167 chance)

If we run some quick math, we can see that if we allocate our entire net worth to this game, the long term expected CAGR is ~(-.4)%:

Where x = 100% (full portfolio allocation):

If we wanted to maximize our expected geometric return, all we need to do is take the derivative of the above formula, and look for the 0, or the local maxima. It turns out it tops out right around a ~30% allocation.

Due to some very convenient math, the average expected geometric return, is basically equal to the median expected geometric return. I.e., by allocating ~30% of our portfolio to this bet, we maximize the 50th percentile outcome.

But why are we maximizing only the 50th percentile of returns? As we discussed before, if we are solving for the betterment of all alternate outcomes, we need to maximize a wider range of outcomes. In finance, the nomenclature to discuss this topic is Value at Risk (or VaR). VaR is shorthand for how much money you could lose on the 5th percentile of outcomes.

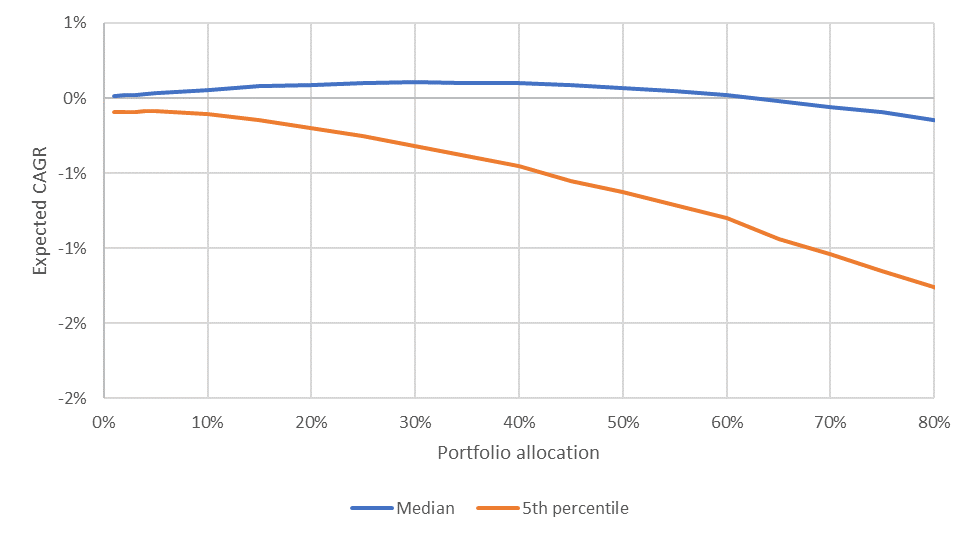

But Kelly can help here. In the chart below, what we see is the expected long term CAGR (y-axis) in both the 50th and 5th percentiles, based on varying portfolio allocations (x-axis):

As you can see, the median portfolio allocation is maximized right around the ~30% allocation range. In contrast, the 5th percentile allocation is maximized at a ~5% allocation.

This is the first reason practitioners allocate a portion of Kelly—it maximizes a lower percentile outcome, reducing the risk across more alternative universes. However, it does this at the cost of the 50th percentile.

This is a good introduction to a theme that will appear often in my work: it is more important to optimize your portfolio for robustness than it is to optimize for returns. You will always make money in the best of outcomes, but what happens in the worst of outcomes is equally important, and yet often overlooked.

Unknown risks, black swans, and sh*! hitting the fan

Being a good investor is almost always less about managing returns as it is managing risk. But while some risks are knowable and quantifiable (both in terms of probability and implications), there are also Black Swans—NNT’s term for unknown-unknowns. Good investors have the humility to understand that they cannot foresee all risks.

Building a portfolio is an art of balancing a maximized CAGR, while avoiding the unforeseeable risks of the world. Under-sizing Kelly is just one possible lever investors have to protect themselves.

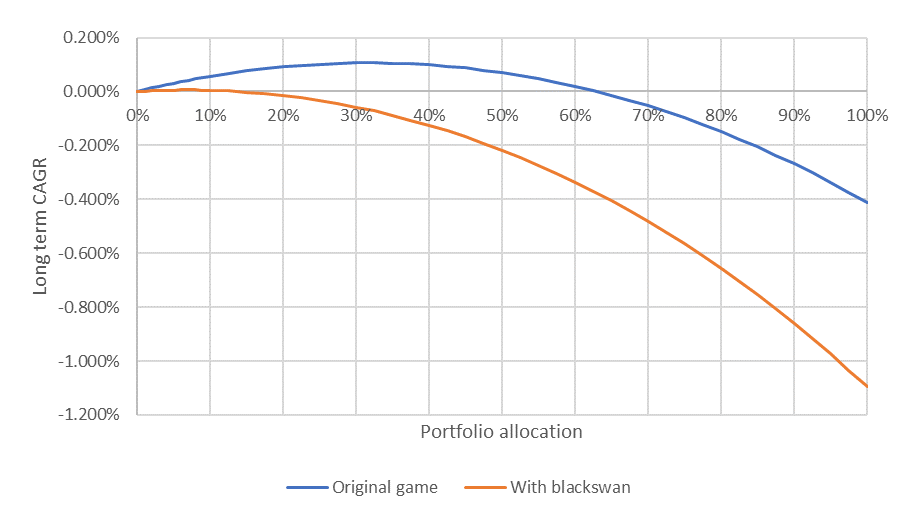

Let’s use an example. Imagine the same game as above, but before you play a 100 sided dice is rolled, and in 1/100 of all outcomes, you lose 50%. Below we can see the expected 50th percentile compounding rate for both the original game we described above, as well as the modified version:

As we can see, the original game maximizes at a ~30% allocation, while the game with a black swan doesn’t maximize until you hit a ~7% allocation.

There are two implications here. The first is when analyzing a potential investment, even very unlikely tail risks can have significant impacts to our return profile. And second, even if we are not aware of potential tail risks, there is always a chance there is an unkown-unkown. To adjust for this, we should scale back our allocation, and leave a margin of safety in case a downside risk does end up playing out.

Uncertainty, best guesses, and being wrong

Gambling games are the basis of all statistics. But casinos are wholly unlike any other game in the real world, because in life the probabilities are not known. Sure, we can take our best guess at estimating. We can try and understand what catalysts would change perceptions and how. But at the end of the day, a game with known odds is going to be very different to a game with uncertainty.

Kelly is one of the many calculations that has its roots in gambling. When we assign probabilities and outcomes in Kelly, we have to acknowledge that we don’t actually know what will happen. The tail risks we discussed previously are a part of this, but the bigger problem is that even for the risks we’ve identified we can miscalculate the probability of them occurring.

The solution here once again is not to have perfect foresight, but instead to construct the portfolio such that it is robust in the face of uncertainty. And we can do that by understanding the convexity in the Kelly Criterion.

Let’s go back to the original game, but this time also look at what happens if we were incorrect in our assessments of both the likelihood, and the impact of tail risks.

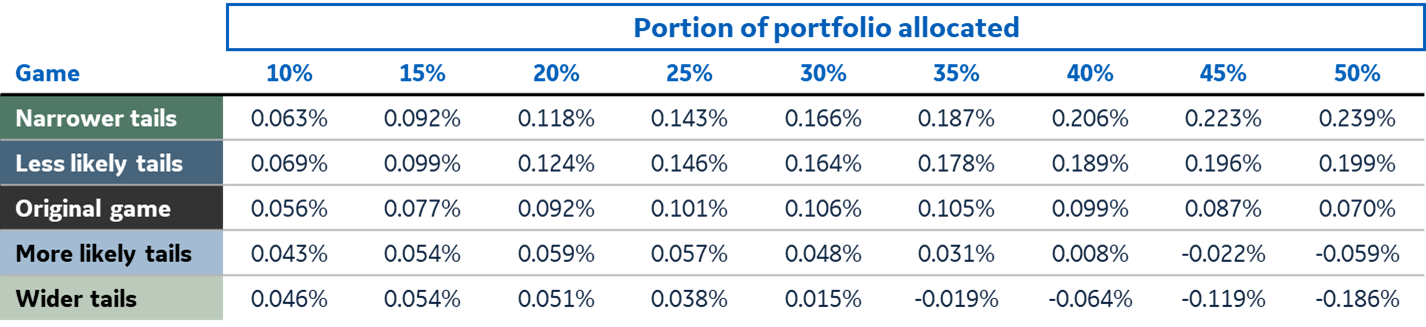

To do this, we can simply add additional games that tweak our original game, but with slightly varying outcomes and probabilities:

If we drew the expected median CAGR for a corresponding proportional allocation of each of the games above, we result in the following chart:

As we can see, the variance of the outcome increases significantly as we go further and further away from a 0% allocation. The table below summarizes a number of points on the chart above:

Directionally, we can see a trend emerging here. If we reduce our allocation from the Kelly implied ~30% to something lower (perhaps ~20%), we only impact expected outcome (the original game) by -1%. However, we directionally increase the values below our game more significantly-- by 3 – 4%. In other words the impact of uncertainty is reduced in exchange for a lower return based on our forecasted outcomes.

Trading perfectly optimized returns for a more robust outcome is most often a good thing. The world is wildly difficult to predict, and it is almost always beneficial to have a protected downside. Understanding and adapting Kelly allows us to do just that.

Like this post? Please consider sharing it!

I have borrowed this game liberally from Mark Spitznagel’s book Safe Haven Investing